Operating a solo business requires a distinct set of skills compared to managing a large corporation. You are the strategy, the execution, and the safety net all at once. When the economic landscape shifts, the ripple effects are immediate. There is no corporate buffer to absorb the shock. For the independent practitioner, understanding these shifts is not optional; it is the foundation of longevity.

This guide explores how to use a structured SWOT analysis to fortify your practice against volatility. We will look at internal capabilities and external pressures without relying on specific tools or software. The focus remains on strategy, mindset, and operational resilience.

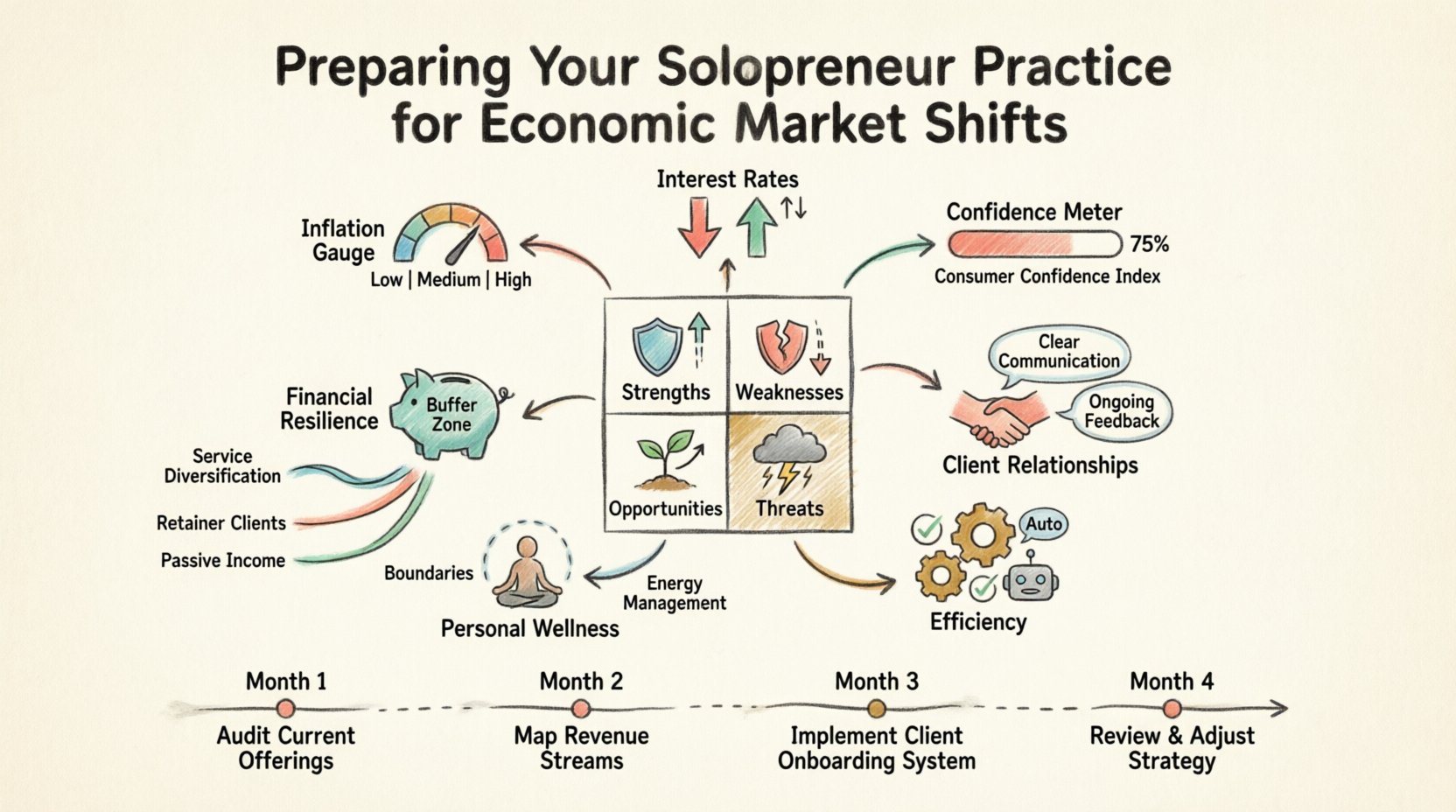

Understanding the Current Economic Landscape 🌍

Economic shifts are not always dramatic crashes. Sometimes they are subtle, creeping changes in interest rates, inflation, or consumer spending habits. As a solopreneur, you are often the first to feel these changes when a client hesitates to sign a contract or delays payment.

Historical data shows that independent businesses face unique challenges during downturns. They lack the cash reserves of larger entities. They often rely on a smaller client base. A single departure can impact a significant portion of revenue.

To navigate this, you must be proactive. Waiting for the market to stabilize is a strategy that often leads to reactive scrambling. Preparation involves knowing your numbers and understanding your position relative to the market.

- Interest Rates: Higher rates make borrowing expensive. Clients may pause expansion projects.

- Inflation: Costs for your own operations may rise. You must adjust pricing without losing demand.

- Consumer Confidence: When people feel uncertain, discretionary spending drops. Your services might be viewed as optional rather than essential.

Recognizing these macro factors helps you anticipate changes in client behavior before they happen.

The SWOT Framework for Independent Practices 🧠

SWOT stands for Strengths, Weaknesses, Opportunities, and Threats. While often associated with large corporations, this framework is incredibly powerful for solo practitioners. It forces you to look at your business objectively.

Unlike a large company, you have direct access to all the data needed for this analysis. You know your cash flow, your workload, and your client relationships intimately. This transparency allows for a more accurate assessment.

Here is how to structure your analysis for an economic shift:

1. Strengths (Internal)

Strengths are what you do well. In a volatile market, agility is a primary strength. You can pivot faster than a department within a large organization. You do not need board approval to change your pricing model or service offering.

- Low Overhead: You do not have a large payroll or expensive office lease. Your burn rate is low.

- Agility: You can test new services quickly without bureaucratic delays.

- Direct Client Access: You build relationships directly. This fosters loyalty during tough times.

- Niche Expertise: Deep specialization often allows you to command higher rates even when the market is tight.

Identify these assets. When the market shifts, lean on these strengths to maintain stability.

2. Weaknesses (Internal)

Weaknesses are internal gaps that could hinder your performance. In an economic downturn, these gaps become vulnerabilities. You must address them before a crisis hits.

- Cash Reserves: Do you have enough savings to cover six months of operating expenses?

- Client Concentration: If one client provides 50% of your revenue, you are at risk if they leave.

- Process Gaps: Do you rely on manual workflows that could fail under stress?

- Skill Gaps: Are you missing skills that are currently in high demand?

Be honest here. Ignoring weaknesses does not make them disappear. It only makes them more dangerous when the economy turns.

3. Opportunities (External)

Opportunities are external chances to grow or improve. Economic shifts often create new needs. When budgets are tight, clients need efficiency. When hiring freezes happen, they need contractors.

- Cost Reduction Services: Clients need help cutting costs. Can you offer consulting on this?

- Market Gaps: Competitors may pull back. Can you fill the void with your capacity?

- New Niches: Shifts in regulation or technology may create demand for new services.

- Retention: Existing clients may need more support than usual to navigate changes.

Scanning the horizon for these opportunities allows you to turn a threat into a revenue stream.

4. Threats (External)

Threats are external factors that could cause trouble. These are often outside your control, but you can prepare for them.

- Competitor Pricing: New entrants may undercut prices to gain market share.

- Client Budget Cuts: Marketing and consulting budgets are often the first to go.

- Regulatory Changes: New laws may increase your compliance burden.

- Technology Disruption: Automation tools may replace certain tasks you currently perform.

Mapping these threats helps you create contingency plans. You cannot stop the threat, but you can reduce its impact.

Visualizing Your SWOT Analysis 📊

Writing down the analysis is the first step. Organizing it visually helps you see the connections between your internal state and external pressures. Use a table to map out your current situation.

| Category | Key Focus Area | Current Status | Impact of Economic Shift |

|---|---|---|---|

| Strengths | Agility | High | Allows rapid adaptation to price changes |

| Weaknesses | Cash Flow | Medium | Increases risk during payment delays |

| Opportunities | Client Education | Low | High demand for cost-saving advice |

| Threats | Client Churn | Medium | Revenue volatility increases |

This table is a living document. Update it quarterly. As the market changes, the status of each item will shift.

Building Financial Resilience 💰

Financial health is the bedrock of a solopreneur practice. When the economy shifts, cash flow becomes the priority. You cannot pivot if you cannot pay your bills.

1. Establishing a Cash Buffer

Aim to save enough to cover at least three to six months of fixed expenses. This is your runway. It gives you the time to find new work without panic.

- Separate Accounts: Keep business and personal funds distinct. It makes tracking easier.

- Automated Savings: Set up automatic transfers to a high-yield account whenever income is received.

- Expense Audit: Review your fixed costs. Can you reduce them? Negotiate vendor rates or switch to usage-based models.

2. Diversifying Revenue Streams

Relying on a single type of income is risky. If one stream dries up, the practice stalls. Diversification does not mean doing everything. It means having multiple sources of payment.

- Retainers: Move clients from project-based to monthly retainers. This guarantees baseline income.

- Productized Services: Create fixed-scope offerings that are easier to sell during uncertainty.

- Passive Income: Develop digital products or courses that generate revenue without active time.

3. Pricing Strategy Adjustments

How you price your services matters. In an inflationary environment, your costs rise. You must adjust prices to maintain margins.

- Value-Based Pricing: Charge based on the value delivered, not the hours spent. This insulates you from time inefficiencies.

- Contract Clauses: Include clauses that allow for price adjustments based on inflation or scope changes.

- Upfront Deposits: Require larger deposits to improve cash flow and reduce risk.

Client Strategy and Relationship Management 🤝

Your clients are your lifeline. Their financial health is tied to yours. During economic shifts, their needs change. You must adapt your relationship management to support them.

1. Communication Transparency

Do not hide the challenges. Open communication builds trust. If you are adjusting prices or changing terms, explain why. Clients appreciate honesty.

- Regular Check-ins: Schedule meetings to discuss their goals and challenges.

- Proactive Updates: Tell them about market trends that might affect their business.

- Feedback Loops: Ask what is working and what is not. Adjust your delivery accordingly.

2. Retention Over Acquisition

It is often cheaper to keep a client than to find a new one. In a tight market, acquisition becomes more expensive. Focus on maximizing the lifetime value of existing clients.

- Upsell Strategically: Offer additional services that solve current problems.

- Referral Programs: Encourage happy clients to refer others.

- Priority Support: Give existing clients priority access to your time.

3. Client Segmentation

Not all clients are equal. Some are more resilient than others. Segment your client base to understand who is at risk.

- High Stability: Essential services clients who pay on time.

- Medium Stability: Clients who might delay payment but are reliable.

- High Risk: Clients in industries facing downturns. Prepare contingency plans for these.

Operational Efficiency and Process Optimization ⚙️

Efficiency becomes critical when margins are thin. You need to do more with less. This does not mean cutting corners. It means removing waste.

1. Workflow Audit

Review your daily tasks. Identify steps that do not add value. Eliminate or automate them.

- Documentation: Create standard operating procedures. This reduces the time spent on repetitive tasks.

- Batching: Group similar tasks together to maintain focus and reduce context switching.

- Outsourcing: Delegate administrative tasks to virtual assistants or contractors. Focus on high-value work.

2. Technology Leverage

You do not need expensive software. Use tools that integrate well and reduce manual work. Focus on functionality, not features.

- Automation: Use simple automation to handle invoicing or scheduling.

- Cloud Storage: Ensure files are accessible from anywhere to allow remote work flexibility.

- Communication: Use reliable channels to keep clients updated without phone tag.

Personal Resilience and Mental Health 🧘

The stress of managing a business alone is significant. Economic uncertainty adds pressure. Your mental health is a business asset. If you burn out, the business stops.

- Boundaries: Set clear work hours. Disconnect after work to recharge.

- Support Network: Connect with other solopreneurs. Sharing experiences reduces isolation.

- Continuous Learning: Stay updated on industry trends. Knowledge reduces anxiety about the unknown.

- Health: Prioritize sleep, exercise, and nutrition. Physical health supports mental stamina.

Monitoring Indicators for Future Shifts 🔍

You cannot predict the future, but you can watch for signals. Keep an eye on specific indicators that suggest a change is coming.

1. Economic Indicators

- Inflation Reports: Watch for changes in consumer price indices.

- Employment Data: Rising unemployment often means less spending power for clients.

- Interest Rate Decisions: Central bank decisions affect borrowing costs for your clients.

2. Industry Signals

- Job Postings: A drop in hiring within your niche indicates a slowdown.

- Competitor Activity: Are competitors launching new products or cutting prices?

- Client Inquiries: Are clients asking for discounts or smaller scopes?

3. Internal Metrics

- Lead Conversion: A drop in conversion rates suggests market hesitation.

- Payment Delays: If clients pay slower, cash flow pressure is increasing.

- Client Churn: An increase in cancellations requires immediate attention.

Implementing the Action Plan 🚀

Knowledge is only useful if applied. Create a schedule to implement these strategies. Break the plan into manageable steps.

- Month 1: Complete the SWOT analysis and audit cash flow.

- Month 2: Implement pricing adjustments and review contracts.

- Month 3: Launch new service offerings based on opportunities found.

- Month 4: Review progress and adjust the plan based on results.

Consistency is key. Do not try to change everything overnight. Small, steady improvements compound over time.

Final Thoughts on Adaptability 🌱

The goal is not to predict every shift perfectly. The goal is to build a practice that can withstand them. Solopreneurs have the advantage of speed. When you spot a change, you can move faster than a corporation.

Use your SWOT analysis as a compass. It guides your decisions when the path is unclear. Focus on your strengths, fix your weaknesses, seize opportunities, and mitigate threats. This disciplined approach creates stability.

Stay informed. Stay flexible. Your practice is your responsibility. With the right preparation, you can navigate economic shifts with confidence and maintain growth.