Financial stability is the bedrock of any sustainable enterprise. When organizations conduct a comprehensive SWOT analysis, they often uncover vulnerabilities that extend beyond market positioning and into the core mechanics of liquidity. Cash flow risks identified during this strategic assessment require immediate and calculated attention. Ignoring these signals can lead to operational paralysis, even when profitability appears strong on paper.

This guide details a structured approach to addressing liquidity threats. It moves beyond theoretical advice to provide actionable frameworks for stabilizing cash positions. By integrating financial rigor with strategic insight, businesses can transform identified risks into opportunities for resilience.

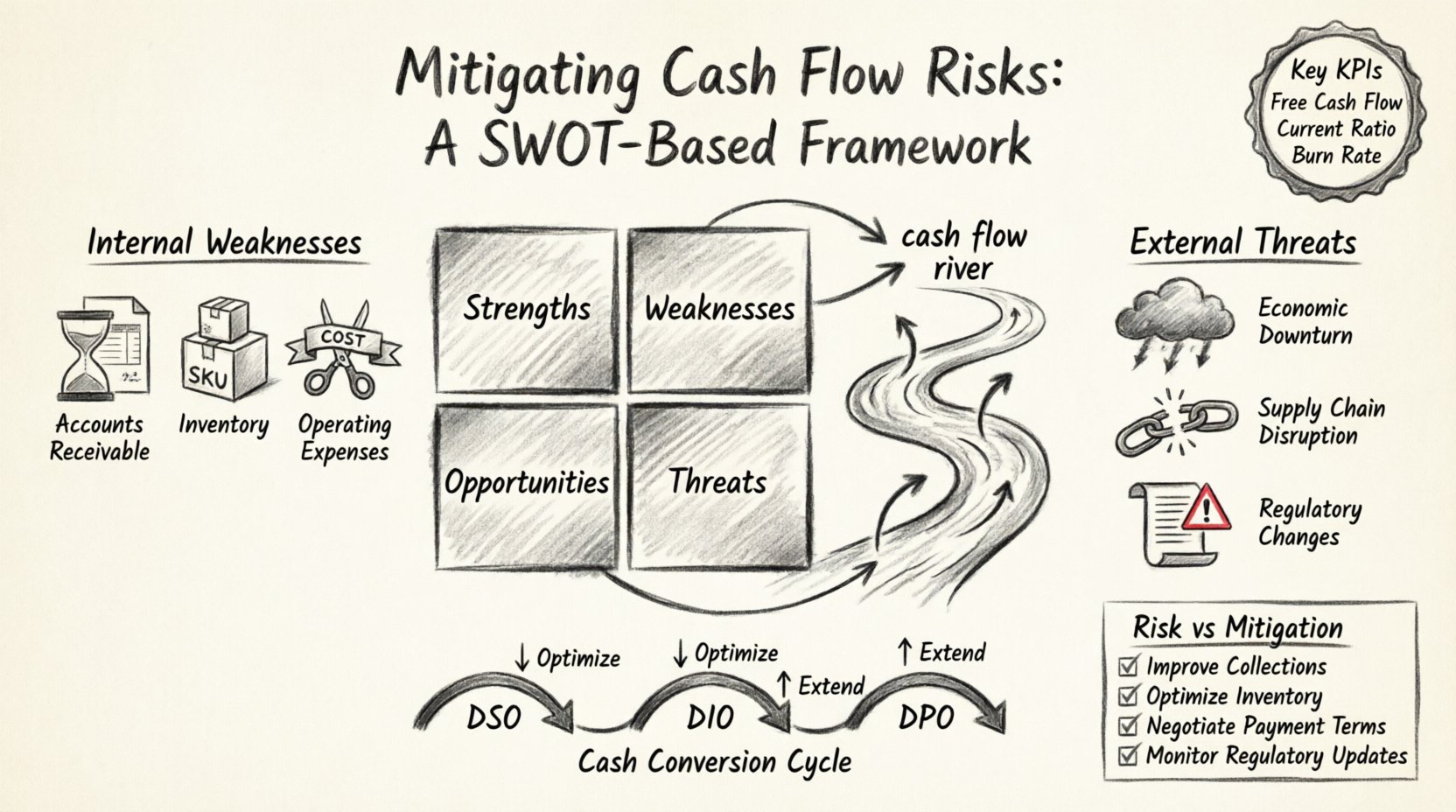

📊 The Intersection of Strategic Planning and Liquidity

A SWOT analysis is traditionally viewed as a marketing or strategic tool. However, when applied to financial health, it reveals critical dependencies. Strengths may provide cash buffers, while threats might expose structural fragility. Weaknesses often point to operational inefficiencies that drain working capital. Threats represent external pressures that can tighten liquidity.

Understanding the connection between these four quadrants and cash flow is the first step in mitigation. Many organizations mistake revenue for cash. Revenue recognizes earnings; cash flow recognizes movement. A robust strategy must account for the timing differences between invoicing, payment collection, and vendor disbursements.

- Strengths (S): Internal assets that generate cash or reduce outflows.

- Weaknesses (W): Internal gaps that consume cash faster than it is generated.

- Opportunities (O): External chances to improve cash inflow or reduce costs.

- Threats (T): External factors that could disrupt cash availability.

When risks are identified, they do not exist in a vacuum. They interact with the broader economic environment. For instance, a weakness in collection processes becomes a threat when the market tightens. Conversely, a strength in product demand can mitigate a threat of rising interest rates.

⚠️ Addressing Internal Weaknesses in Cash Management

Internal weaknesses are the most direct targets for immediate intervention. These are factors within the organization’s control that negatively impact liquidity. Common weaknesses include delayed billing cycles, excessive inventory holding, and reliance on short-term debt.

1. Optimizing Accounts Receivable

Delays in collecting payments create artificial cash shortages. Even profitable companies can fail if cash remains stuck in accounts receivable. Addressing this requires a review of credit policies and collection workflows.

- Review Credit Terms: Ensure payment terms align with industry standards and customer capabilities.

- Invoice Accuracy: Errors in invoicing cause disputes and delays. Verify data before sending.

- Automated Follow-ups: Implement systematic reminders for overdue accounts.

- Discounts for Early Payment: Incentivize customers to pay faster with defined early payment terms.

2. Managing Inventory Levels

Inventory represents cash tied up in stock. Overstocking increases holding costs and risk of obsolescence. Understocking risks lost sales. The goal is a balanced approach that supports operations without draining reserves.

- ABC Analysis: Categorize inventory by value and turnover rate.

- Just-in-Time Methods: Align purchasing with production schedules to reduce storage costs.

- Regular Audits: Identify slow-moving items and clear them through promotions or disposal.

- Supplier Coordination: Negotiate consignment stock arrangements to delay cash outflow.

3. Controlling Operating Expenses

Fixed costs drain cash regardless of revenue performance. Identifying non-essential expenditures is crucial during risk mitigation phases.

- Vendor Contract Review: Renegotiate terms with suppliers to extend payment windows.

- Subscription Audit: Eliminate unused software licenses or service subscriptions.

- Energy and Utilities: Implement efficiency measures to reduce monthly overhead.

- Outsourcing Non-Core Functions: Shift fixed labor costs to variable costs where appropriate.

🌪️ Neutralizing External Threats to Cash Flow

External threats are forces outside the organization that can disrupt financial stability. These include economic downturns, regulatory changes, and competitor actions. While these cannot be controlled, their impact on cash flow can be managed.

1. Economic Downturns

Recessionary periods often lead to reduced customer spending and tighter credit markets. Preparing for this requires building reserves before the downturn occurs.

- Build Cash Reserves: Maintain a buffer of three to six months of operating expenses.

- Diversify Revenue Streams: Avoid reliance on a single client or product line.

- Flexible Pricing Models: Offer tiered pricing to retain customers during economic stress.

2. Supply Chain Disruptions

Dependency on single-source suppliers creates vulnerability. If a supplier fails, production halts, and cash inflow stops.

- Multisourcing: Qualify multiple vendors for critical components.

- Strategic Stockpiling: Hold safety stock for essential materials during stable periods.

- Supplier Financial Health: Monitor the financial stability of key partners.

3. Regulatory Changes

New tax laws or compliance requirements can alter cash flow timing. Proactive planning is necessary to avoid surprise liabilities.

- Compliance Audits: Regularly review tax obligations and accounting practices.

- Government Grants: Identify available funding to offset compliance costs.

- Legal Consultation: Engage experts to interpret new regulations early.

🚀 Leveraging Strengths for Liquidity Reserves

Strengths are internal assets that provide a competitive advantage. In the context of cash flow, strengths are opportunities to generate surplus funds. These funds should be directed toward risk mitigation strategies.

1. High-Margin Products

Products with high profit margins generate more cash per unit sold. Prioritizing these can improve overall liquidity.

- Pricing Strategy: Align pricing to reflect the true value and cost of high-margin items.

- Resource Allocation: Direct marketing spend toward top-performing offerings.

- Cost Reduction: Focus on minimizing variable costs for these specific products.

2. Strong Customer Relationships

Long-term clients often provide predictable revenue. This predictability allows for better cash flow forecasting.

- Retention Programs: Implement loyalty incentives to reduce churn.

- Long-Term Contracts: Secure multi-year agreements to stabilize income.

- Upselling: Leverage trust to introduce complementary services.

3. Efficient Processes

Operational efficiency reduces waste and improves cash conversion. Streamlined workflows mean less capital is tied up in production delays.

- Workflow Automation: Use technology to reduce manual errors and time.

- Lean Methodologies: Eliminate steps that do not add value to the customer.

- Training: Invest in staff development to improve speed and accuracy.

🛠️ Tactical Adjustments to Cash Conversion Cycles

The Cash Conversion Cycle (CCC) measures the time between spending cash on inventory and receiving cash from sales. Shortening this cycle frees up capital for other uses. This is a critical lever for managing risk.

1. Shortening the Days Sales Outstanding (DSO)

DSO indicates how long it takes to collect payment after a sale. Lowering this number improves liquidity.

- Electronic Invoicing: Reduce mailing times and processing delays.

- Payment Gateways: Accept multiple payment methods for customer convenience.

- Factoring: Sell receivables to a third party for immediate cash (if terms allow).

2. Extending Days Payable Outstanding (DPO)

DPO measures how long the business takes to pay its suppliers. Extending this preserves cash longer without incurring penalties.

- Negotiated Terms: Move from Net 30 to Net 60 where possible.

- Volume Discounts: Trade faster payment for price reductions.

- Strategic Timing: Align payments with cash inflow dates.

3. Reducing Days Inventory Outstanding (DIO)

DIO reflects how long inventory sits before being sold. Faster turnover means less cash is locked in stock.

- Dynamic Pricing: Adjust prices based on demand to move stock.

- Pre-Sales: Sell products before they are manufactured to reduce holding time.

- Dropshipping: Transfer inventory holding to suppliers where feasible.

📋 Risk vs. Mitigation Mapping

The following table summarizes common cash flow risks identified in SWOT analysis and their corresponding mitigation strategies. This serves as a checklist for financial leaders.

| Risk Category | SWOT Origin | Mitigation Strategy | Impact on Cash |

|---|---|---|---|

| High Inventory Costs | Weakness | Implement Just-in-Time ordering | Reduces capital tied in stock |

| Slow Collections | Weakness | Automated dunning and credit checks | Accelerates cash inflow |

| Market Competition | Threat | Differentiate via premium service | Protects margins and pricing power |

| Economic Recession | Threat | Build 6-month cash reserve | Ensures operational continuity |

| High Customer Churn | Weakness | Launch retention and loyalty programs | Stabilizes recurring revenue |

| Supplier Price Hikes | Threat | Lock in long-term pricing contracts | Controls variable cost volatility |

| Excess Cash Reserves | Strength | Invest in short-term liquid instruments | Generates interest income |

| Strong Brand Equity | Strength | Leverage for premium pricing | Increases margin per unit |

📈 Monitoring Frameworks for Sustained Stability

Once mitigation strategies are in place, continuous monitoring is essential. Cash flow is dynamic, and risks can re-emerge if not tracked. Establishing a framework ensures early detection of new issues.

1. Key Performance Indicators (KPIs)

Define specific metrics to track the health of the cash position. Regular reporting allows for timely adjustments.

- Free Cash Flow: Net cash provided by operating activities minus capital expenditures.

- Current Ratio: Current assets divided by current liabilities.

- Operating Cash Flow Ratio: Cash flow from operations divided by current liabilities.

- Burn Rate: The rate at which a company spends its cash reserves.

2. Cash Flow Forecasting

Forecasting provides a view of future liquidity. It allows leadership to anticipate shortfalls before they occur.

- 13-Week Rolling Forecast: A detailed short-term view of cash inflows and outflows.

- Scenario Planning: Model best-case, worst-case, and most-likely scenarios.

- Weekly Reviews: Update forecasts based on actual performance.

3. Governance and Accountability

Clear ownership of cash management responsibilities ensures actions are taken. Designate specific roles for financial oversight.

- Treasury Function: Assign a dedicated role or team to manage liquidity.

- Cash Committee: Form a cross-functional group to review risks monthly.

- Approval Limits: Set spending thresholds to prevent unauthorized outflows.

🔍 Final Considerations for Long-Term Health

Mitigating cash flow risks is not a one-time event. It is an ongoing discipline that requires vigilance and adaptation. The strategies outlined above form a foundation for financial resilience.

Organizations must remain agile. Market conditions change, and what works today may not work tomorrow. Regularly revisiting the SWOT analysis ensures that financial strategies stay aligned with operational realities.

By focusing on internal controls, external preparedness, and continuous monitoring, businesses can navigate uncertainty. Cash flow management becomes less about survival and more about strategic growth. This shift in perspective empowers leaders to make decisions that secure the future of the enterprise.

Remember that liquidity is a leading indicator of health. Profitability is a lagging indicator. Prioritizing cash flow ensures that the organization remains solvent while pursuing its long-term vision. Implement these measures systematically to build a robust financial structure capable of withstanding market volatility.

The path to stability lies in detail. Every invoice, every inventory item, and every vendor contract contributes to the overall financial picture. Attention to these details creates a shield against risk. With a clear plan and disciplined execution, cash flow risks transform from threats into manageable variables.